India’s millennials think nothing of switching from an Ayurvedic face wash to a Korean sheet mask in the same week, and ordering both directly from the brands’ Instagram page. That “tap-and-try” mindset is what’s turbocharging India’s direct-to-consumer (D2C) and new-age consumer brand boom, and Venture Capital is the rocket fuel behind it.

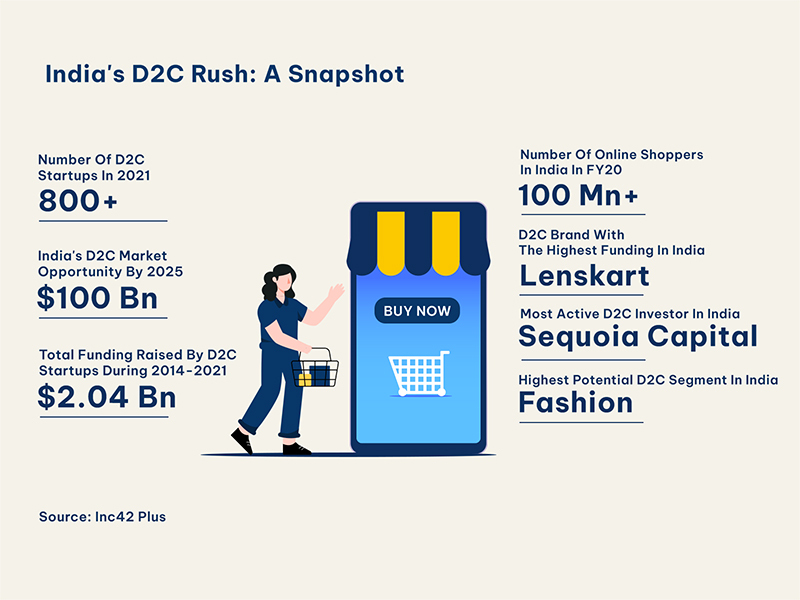

In barely five years, India has gone from a handful of digital-native labels to over 800 D2C brands straddling beauty, fashion, electronics, food, and pet care.

Analysts peg the total D2C market at ₹8-9 lakh crore (approximately US$ 100 billion) by 2025, transforming what was once a curiosity into one of retail’s biggest growth engines.

Why Venture Capitalists Love Indian Consumer Brands

- High-margin adjacencies: A brand that nails one hero Stock Keeping Unit (SKU) (e.g., ayurvedic face wash) can launch serums, masks, and body care at far higher margins.

- Digital-first distribution: No cap-ex-heavy storefronts; Customer Acquisition Cost (CAC) is measurable and optimisable.

- Fast payback periods: Working capital cycles shrink significantly once repeat cohorts are established.

- Massive headroom: Organised retail is under-penetrated; even tier-II/III cities are discovering niche labels via WhatsApp Commerce and influencer live-shopping.

Furthermore, we see three big shifts in the market conditions and upgradation of social infrastructure that set the stage for a seismic change in consumer behaviour patterns:

- Cheap data + UPI turned every smartphone into a mall checkout.

- COVID-era e-commerce adoption made Cash-on-Delivery (COD) sceptics comfortable with online returns and refunds.

- Social-commerce influencers collapsed the marketing funnel—awareness, consideration, and purchase can now happen in a single reel.

What Investors Look for Before Writing That Cheque

- Gross margin north of 60 % on core products.Unit-level profitability by Series A (marketing dollars can wait; unit economics can’t).

- Community moats—not just followers but engaged brand evangelists.

- Omnichannel readiness: Even digital brands must show a plan for modern trade and quick-commerce shelves.

- Supply-chain defensibility: Contract manufacturing is easy to replicate; unique formulations or captive supply can lock in long-term advantage.

Tip for founders: Bring your investor into that private Telegram group or pop-up tasting session. Let them feel the love, not just read the metrics.

Now, let’s delve into the factors that need to be evaluated to better understand the sustainability and the progress of the D2C and consumer brand revolution-

1. The VC Catalyst: More Than Just Money

While founders brought product insight, Venture Capitalists brought the capital and the playbook:

- Early-stage cheques to fund supply-chain experiments.

- Growth-stage rounds that underwrite working-capital-heavy categories like beauty and FMCG.

- Connections to offline retail distributors, CXOs, and export partners that most first-time founders lack.

It shows up in the numbers. After a cautious 2023, Indian VC funding rebounded to US$13.7 billion in 2024, with the consumer and retail sectors among the top magnets.

Within that, pure-play D2C startups still raised a respectable US$757 million in 2024, despite a global reset in valuations.

2. The Policy Boost No One Saw Coming

The Union Budget 2024 scrapped the angel tax on share premiums and slashed the long-term capital gains tax on unlisted shares from 20% to 12.5%. For consumer startups, where early valuations can soar on brand promise alone, those tweaks translate into:

- Larger early-stage rounds without founders worrying about punitive tax notices.

- Easier secondary sales for early angels, recycling capital back into the ecosystem.

3. Challenges on the Road to ₹100 Billion

- High Valuations: Many 2021-era brands still carry frothy caps, complicating fresh rounds.

- Logistics inflation: Rising freight and corrugated-box costs eat into margins.

- Advertising “tax”: iOS privacy changes and Google’s cookie deprecation push CAC up 20-25 %.

- Profit vs. growth dilemma: Public-market investors are unforgiving—ask any emerging startup preparing for an IPO.

4. Navigating the Next Wave: A Practical Playbook for Founders

- Show a path to EBITDA positivity under 24 months. Even growth-stage Venture Capitalists want clear profitability milestones.

- Bet on tech-driven personalisation. AI-guided shade matching, fit analytics, or nutrition chatbots delight users and embed defensible IP.

- Go phygital the smart way. Pop-ups and SIS (shop-in-shop) formats de-risk expensive flagship stores while boosting brand discovery.

- Tier-II/III localisation. Vernacular packaging and regional influencer partnerships can unlock the 400 million-strong “Bharat” consumer cohort.

- Plan your exit early. Whether it’s IPO, strategic sale, or roll-up play, aligning with investor timelines keeps everyone honest.

If the last decade was about proving that Indians will buy premium shampoo online, the next one will be about deepening that relationship through hyper-personalised products, sustainable sourcing, and community-driven innovation.

Venture Capital firms, flush with fresh dry powder and buoyed by regulatory tailwinds, are already marking consumer tech as a core thesis for 2025-27 funds. Combine that with the sheer diversity of India’s demographics—Gen Z influencers in Mumbai, health-conscious parents in Indore, and vegan pet-owners in Kochi—and you get a market that’s too big, too varied, and too aspirational to ignore.

For founders, the message is clear: build a brand that people trust, back it with metrics that Venture Capital firms respect, and the capital will follow. Do that, and you’re not just selling beauty products or appliances—you’re participating in India’s most exciting consumer revolution yet.