In the high-stakes theatre of early-stage consumer investing, a pitch deck is more than a presentation; it is a window into a brand’s future. Every founder walks into a room hoping to showcase a “unicorn” in the making, but seasoned investors are trained to look past the polish. They scan for the subtle cracks in the foundation and early signals that indicate whether a brand can survive operational pressure, capital cycles, and consumer unpredictability long before it reaches a Tier II household or the screens of a million Gen Z shoppers.

Most startups do not fail in the pitch room because their ideas are weak. They fail because something feels off. It could be a number that does not reconcile. A market story that sounds borrowed rather than lived. Or a founder narrative that is ambitious but disconnected from execution reality. Investors may not always articulate it clearly, but they sense risk early. And once doubt sets in, momentum is hard to regain.

Hence, understanding what deters investors is not about avoiding mistakes; it is about building businesses that signal clarity, discipline, and long-term intent from day one.

The Red Flags and Risks That Deter Investors

Across stages and sectors, certain warning signs repeatedly show up as deal breakers. These are not theoretical concerns; they are rooted in how real businesses have struggled or failed.

1. Growth Without Economic Depth

Rapid topline growth often excites founders, but investors look one layer deeper.

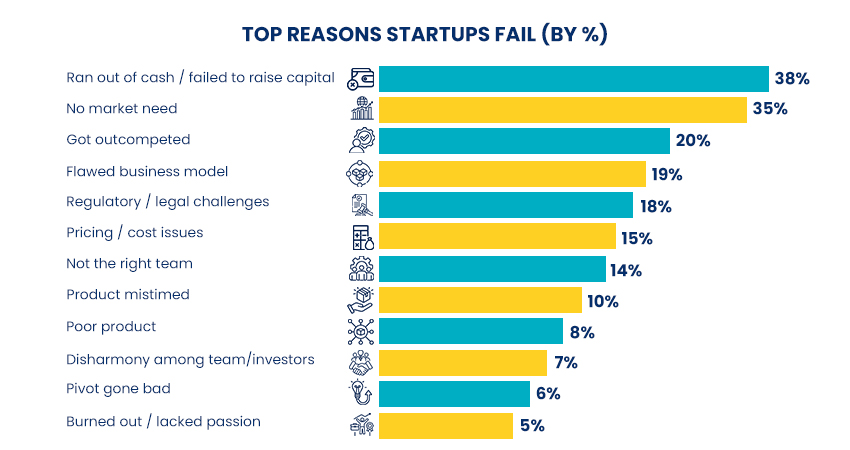

According to CB Insights, 38% of startups fail due to cash shortages, while another 15% fail due to pricing and cost-related issues. When founders cannot clearly explain unit economics, contribution margins, or customer payback cycles, growth becomes a risk rather than an asset.

This is especially critical in consumer businesses, where scaling inefficient economics only magnifies losses. India’s post-2021 funding correction made this clearly visible. Several high-growth consumer startups and D2C brands expanded aggressively through discounts and paid acquisition, only to see repeat rates stagnate and burn rates spike once capital became expensive. As funding tightened, growth narratives collapsed under the weight of weak fundamentals.

2. Shallow Understanding of the Consumer

Another major red flag is when founders describe their customers only in demographic terms.

Investors increasingly expect a deeper understanding and clarity on consumer behaviour. They want to know the trigger moments, usage frequency, emotional drivers, and substitution behaviour. A founder who says “everyone is our customer” signals weak market focus.

Research by Nielsen shows that brands with sharper consumer segmentation and insight-driven positioning are significantly more likely to scale sustainably in competitive categories. In contrast, several consumer startups that stalled did not fail due to a lack of demand, but because the product did not fit into a clear usage habit or cultural context.

3. Overdependence on One Channel or One Customer

Channel concentration is another major risk signal.

Businesses that rely heavily on a single distribution channel or one large buyer expose themselves to concentrated risk. During diligence, investors often flag startups whose revenue is more than 30-40% from a single platform, marketplace, or enterprise client. Any algorithm change, commission revision, or partnership loss can significantly impact survival.

This risk has played out globally, particularly for D2C brands. Brands overly dependent on paid digital acquisition faced rising CACs as platforms matured and competition intensified. Forbes reports that customer acquisition costs for many digital-first brands increased by more than 60% between 2017 and 2022, compressing margins and slowing growth.

4. Founder Narratives That Avoid Hard Truths

Optimism is expected; evasion is not.

Investors become cautious when founders gloss over challenges, excessively blame external factors, or avoid discussing past mistakes. According to the Harvard Business Review, investors value a founder’s self-awareness and learning ability more than flawless execution history. A lack of transparency raises concerns about governance, decision-making, and how founders will behave when the business faces inevitable turbulence. Founders who cannot clearly articulate what went wrong in the past often struggle to convince investors they can navigate what will go wrong next. In contrast, honest reflection signals maturity, accountability, and the ability to adapt under pressure.

5. Cap Table and Governance Shortcuts

Early shortcuts often surface later as structural problems.

Overdilution at the Seed stage, unclear equity splits, or granting equity to inactive advisors can make future funding difficult. What founders may see as early hustle, investors see as poor planning and governance risk. In India, several startups have struggled to raise Series A or B rounds due to fragmented ownership and unresolved founder equity issues. This is why cap table hygiene has become a key diligence filter. Industry guidance suggests that when founder ownership drops below 15-20% by Series B, investors worry about reduced skin in the game. Informal equity promises or delayed ROC filings further slow or stall investment discussions.

What Founders Can Learn to Become Green Flags

The good news is that most red flags are not permanent. They are signals. And signals can be read, understood, and corrected with intent and discipline. Many of today’s strongest consumer businesses were not built without early mistakes. They were built by founders who learned faster than the risks compounded.

-

Build for Contribution Before Scale

Founders who earn investor confidence focus early on visibility into contribution margin, even when the numbers are still evolving. They understand where money is made, where it is lost, and what improves with scale.

Several consumer brands that survived the post-2021 funding reset did so by pausing aggressive acquisitions and focusing on fixing unit economics at a city or cohort level. Growth slowed temporarily, but predictability improved. Investors value this restraint because it signals control, not caution.

Scaling becomes meaningful only when every new customer strengthens the business rather than strains it.

-

Go Deeper Than Demographics

Strong consumer founders talk less about age groups and income brackets and more about moments, motivations, and repeat behaviour. They know when their product is chosen, what emotional or functional job it performs, and why a consumer comes back.

Some of India’s most enduring consumer brands were not first movers. They won because they understood habits better. Whether it was daily consumption, festival-driven purchase cycles, or trust-based repeat usage, this depth allowed them to build brands that stuck. Investors read this as long-term brand potential, not short-term demand spikes.

-

Design for Channel Resilience Early

Investors lean in when founders actively reduce single-channel risk. This does not require scale. It requires intent.

Founders who test multiple distribution paths, invest early in retention, or build organic pull alongside paid growth show strategic maturity. Even modest signals, such as repeat orders, offline pilots, or community-driven demand, indicate resilience. In volatile markets, businesses that can adapt their distribution strategies survive longer than those optimised for a single platform.

-

Show Learning, Not Perfection

Investors do not expect flawless execution. They expect honest learning curves.

Founders who openly share what did not work, what changed, and why they pivoted build credibility. Many seasoned investors will say that self-awareness is a stronger predictor of long-term success than early traction. Adaptability matters more than initial certainty, especially in consumer markets where behaviour shifts faster than forecasts.

-

Think Two Rounds Ahead

Clean governance, thoughtful equity structures, and documented decision-making may feel slow in the early days, but they compound trust over time. Founders who treat equity, compliance, and reporting as strategic assets rather than administrative chores reduce friction in future funding rounds.

When basics are in place, due diligence moves faster, conversations stay focused on growth, and credibility builds organically. Investors read this discipline as a signal that the company is designed to scale responsibly, not just chase speed. Businesses that plan for two rounds tend to attract patient capital and stronger, long-term partners.

To conclude, investor rejection is often internalised as a verdict. In reality, it is diagnostic.

Most investors are not reacting to the idea itself, but to risk signals they have seen repeat across market cycles. Founders who learn to treat this feedback as data rather than judgment gain an unfair advantage. They course correct earlier, allocate capital more intelligently, and build businesses that hold up under pressure.

Capital follows clarity. And clarity is built deliberately, through honest metrics, disciplined decisions, and realistic narratives.

The most fundable startups are not the ones without flaws. They are the ones that recognise risk early, address it with intent, and evolve faster than the market around them. As capital becomes more selective and consumers more demanding, resilience will matter more than speed. When founders view red flags as a roadmap rather than a rejection, they are no longer just preparing for the next pitch. They are building businesses capable of enduring cycles, earning trust, and shaping the future of the Indian consumer economy.