If you’ve ever managed a Beauty & Personal Care profit and loss statement, you probably recognize this situation.

Sales are rising and reviews are positive. Your product is reaching customers outside your personal network. You’d expect to feel some relief, but instead, you’re talking to your manufacturer about paying for the next batch, your distributor wants a plan to keep your brand visible, and you’re checking your bank account wondering why cash is still tight.

At this stage, many founders think, “BPC is expensive.”

But a better way to look at it is that BPC is really a shelf business. The product just gets you in the door. Your results depend on where you sell, how you build trust, and how long your cash is tied up before it returns.

And when we talk about shelves, we mean actual shelves, not just a D2C concept:

- the chemist/GT shelf, where trust is borrowed from the shopkeeper and availability is everything,

- the modern trade shelf where visibility is negotiated and measured,

- the marketplace shelf where you’re one scroll away from substitutes, and

- The quick-commerce cart shelf, where decisions happen fast because delivery i (e.l.f. Cosmetics Business Model: TikTok-Driven Dupes and Omnichannel Scale, 2024)s fast.

Quick commerce is now changing how people shop on a large scale. According to Bain’s How India Shops Online 2025, in 2024, over two-thirds of e-grocery orders and one-tenth of e-retail spending happened through quick commerce. The report expects this to grow by more than 40% each year until 2030. (How India Shops Online 2025, 2025) As shopping becomes more immediate, brands have less time to tell their story and need to be clear and direct.

Before diving into the details, it’s helpful to do something many founders overlook: make a basic map.

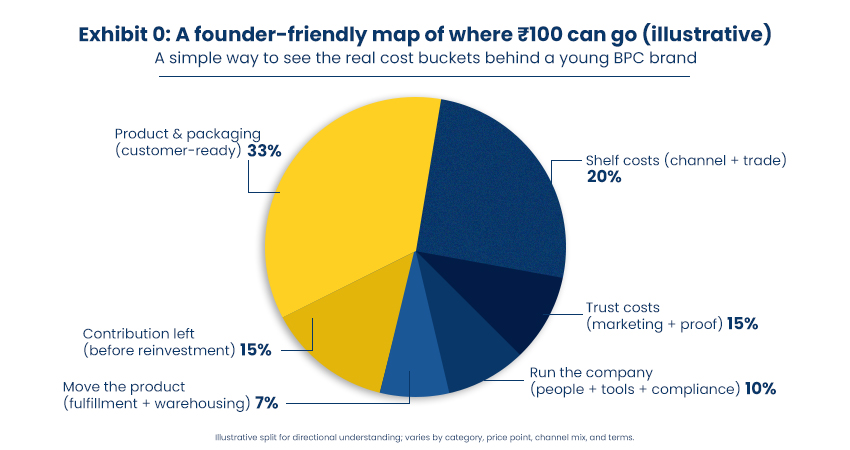

Begin with a simple map: If ₹100 comes in, where does it typically go?

Here’s an easy way for founders to look at it. Suppose your brand makes ₹100 in net revenue after taxes and channel fees. Where does that ₹100 go in a young BPC brand?

A founder-friendly map of where ₹100 can go

This isn’t a one-size-fits-all formula. It’s a reality check. From our experience with many consumer brands, most early-stage BPC businesses find their money gets divided into six main buckets:

- Product & packaging (customer-ready COGS)

- Shelf costs (channel + trade)

- Trust costs (marketing + proof)

- Movement costs (fulfilment + warehousing)

- Running costs (people, tools, compliance)

- Contribution left (what’s left to reinvest, build a buffer, or eventually profit)

Let’s walk through the process in the same order as the product’s journey: make the unit, get it onto shelves, build trust, deliver it reliably, and then wait for the cash to return.

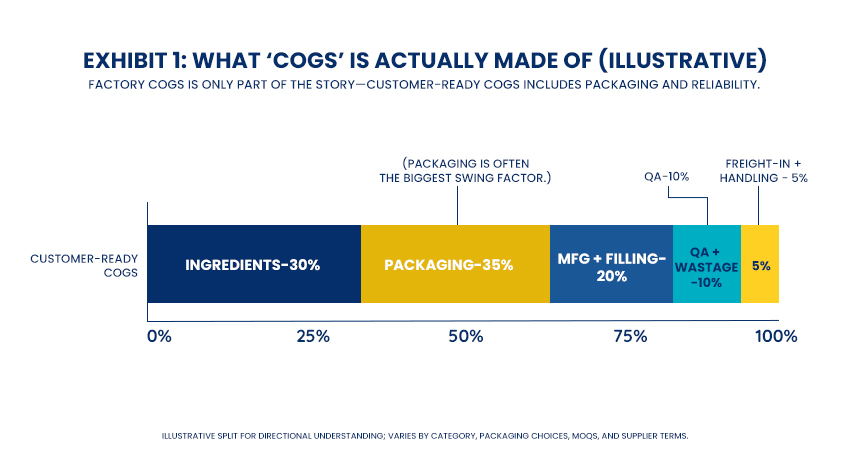

1) Product & packaging: your real COGS is “customer-ready,” not “factory-ready”

Your true cost of goods sold is what it takes to get the product ready for the customer, not just what it costs to make it in the factory.

Most founders know exactly how much it costs to manufacture their product. The real surprise comes from the costs that appear after that.

Customers don’t notice the manufacturing process. They care that the product arrives safely, looks good, feels right, and works as promised. In BPC, if it doesn’t work as expected, you don’t just risk a refund; you also risk a bad rating, a negative review, and losing future sales.

A premium pump can make a serum feel 2X as valuable, but if it leaks during shipping in hot weather, you end up paying for replacements and seeing your product rating drop.

Adding a second carton can help your product stand out in stores, but if you change your claims or price, you might be left with cartons you’ve already paid for but can’t use.

That’s why we encourage founders to track two types of COGS, not just one:

- Factory-ready COGS: what it costs to produce a unit

- Customer-ready COGS: what it costs to get the product to the customer in good condition and without issues

What “COGS” is actually made of?

If your customer-ready COGS is wrong, the brand doesn’t die immediately. It simply becomes more expensive to sell, because your next bucket (trust) has to compensate for a weak experience.

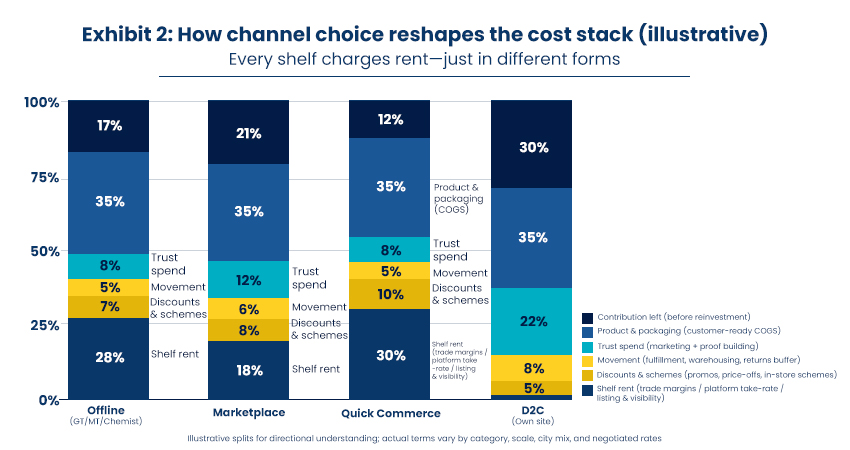

2) Shelf costs: the business is not only a “desire,” it’s a distribution

Every shelf charges rent. Offline shelves charge it in one way; online shelves charge it in another. But none of them are free.

GT + chemist: the shelf of availability and confidence

In general trade and chemists, the buyer doesn’t scroll. The buyer sees what’s stocked, what’s trusted, what the retailer is comfortable recommending. Your costs here are not just margins. They are the operating reality of sales coverage, distributor economics, schemes, and credit cycles. Stock that doesn’t rotate becomes cash trapped in the channel.

Modern trade: the shelf of visibility mechanics

Modern trade can make a brand look “national” quickly, but it comes with commercial structure, listing and visibility mechanics, promotion calendars, and negotiation. Retailers are commercial partners; you need to know your numbers and your story. NielsenIQ’s retailer-facing guidance highlights the importance of being prepared for retailer expectations and negotiations as part of getting onto shelves and staying there.

Marketplaces: the shelf of comparison

Marketplaces turn your brand into a comparison set. Ratings, price-per-ml logic, delivery speed, and authenticity cues do a lot of selling. When those signals are weak, the shelf becomes “paid”, you spend on deals and visibility just to stay in the consideration set.

Quick commerce: the shelf of speed

Quick commerce compresses decision time. The consumer behaves like a responder, not a browser. This is exactly why Bain’s data matters: if q-commerce is already a meaningful slice of e-retail behaviour, brands have to design for “instant legibility,” not just storytelling.

A useful HBR point sits here: DTC brands often win early by exploiting a distribution weakness, but sustaining growth requires evolving the model beyond the initial playbook. In Indian BPC, that evolution often means learning to win across shelves, offline + online, without destroying contribution.

How channel choice reshapes the cost stack?

This exhibit is not saying “don’t sell on X channel.” It’s saying: your channel mix changes what you must pay for to win. Founders get into trouble when they add shelves faster than their unit economics can support.

3) Trust costs: in BPC, marketing is often belief insurance

BPC is personal and visible. A snack that disappoints is forgotten by dinner. A skincare product that irritates your face becomes a story. So buyers don’t just buy product, they buy reassurance.

That reassurance is your proof stack: reviews, demos, before/after evidence, ingredient clarity, claims discipline, and customer support that resolves issues without making the customer feel foolish.

NielsenIQ’s India beauty trends commentary explicitly calls out two shifts that raise the bar for trust: growing demand for ingredient transparency and the increasing influence of digital discovery journeys on what consumers trust and choose. In plain English: promise is cheap; proof is expensive; and consumers are getting sharper about it.

One reason founders think “marketing is burning money” is because they treat proof like a nice-to-have. But if your proof isn’t thick enough, you end up paying for trust through the bluntest tool available: discounts. Discounts can create trials, but they don’t reliably create belief, and they attract the least loyal buyer.

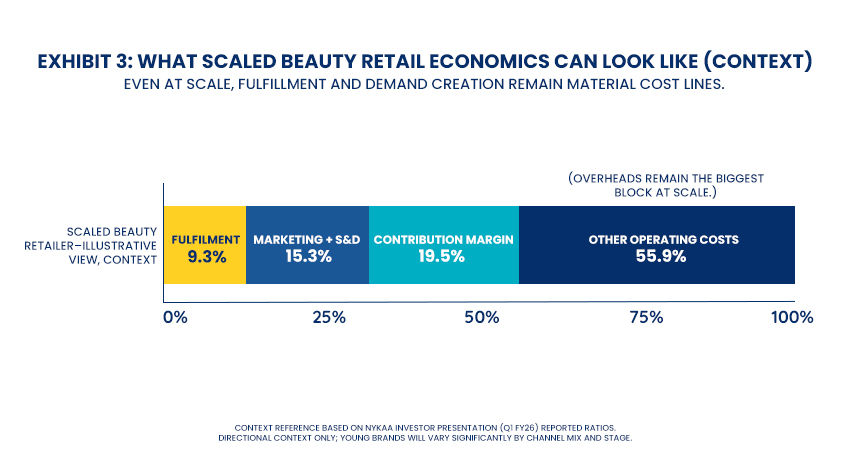

A scaled reference point helps here. Nykaa’s investor disclosures show that even at scale, fulfilment and marketing/selling expenses remain meaningful parts of the model (alongside contribution).

What scaled beauty retail economics can look like?

Don’t copy these numbers. Learn the shape: “sell + serve” costs are structural in beauty.

4) Movement costs: the boring bucket that decides your reputation

Movement costs are everything required to move a unit reliably: warehousing, pick-pack, logistics, returns handling, replacements, and the customer support that sits behind all of it.

This bucket jumps when:

- packaging isn’t stable at scale (leakage, damage, breakage), and

- the catalogue expands (more SKUs = more complexity = more inventory fragmentation).

McKinsey’s omnichannel work makes a broader point that maps cleanly onto consumer brands: fulfilment choices involve trade-offs, and store-based fulfilment can be more expensive for picking/packing than distribution centres, while returns can be cheaper at stores, meaning these costs need to be designed end-to-end, not in silos. Translation for founders: offline can reduce certain frictions, but only if your operating model is built for it.

5) The cash cycle: where good brands quietly suffocate

Here’s the part that creates the “we’re growing but still broke” feeling.

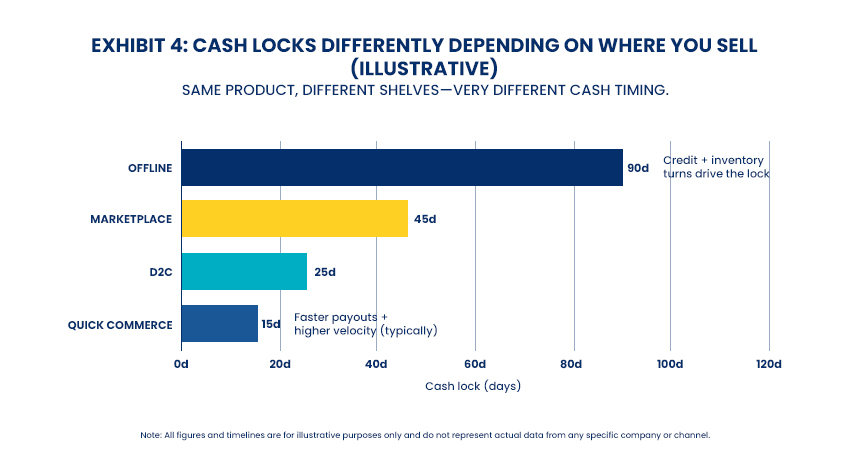

You pay for raw materials and packaging. You wait for production. You hold inventory. You sell. Then you wait for payouts. In offline, you often wait longer because credit is baked into the system. Meanwhile, your next batch needs cash now.

Cash locks differently depending on where you sell

This is why catalogue decisions are cash decisions. Every new SKU is an inventory bet you fund before you know it will move. Too many “maybe” SKUs can trap cash even when the hero SKUs are working.

A simple end summary: one SKU example, all cash components in one view

Let’s make this concrete with a founder-style example. Imagine a ₹499 facewash that you sell across shelves (GT + marketplace + a bit of quick commerce + D2C). We’ll do this in the simplest possible way:

- Assume ₹100 is your net revenue per unit after taxes and after channel cut (so we can compare apples to apples).

- The numbers below are illustrative, but they reflect how cash usually gets pulled.

₹100 comes in. Where can it go?

- ₹33 → Product & packaging (customer-ready COGS): formula + pack + QC/wastage

- ₹20 → Shelf costs: trade margins / platform fees / schemes / visibility mechanics

- ₹15 → Trust costs: content, creators, sampling, performance spend, proof-building

- ₹7 → Movement: warehousing + shipping + returns/replacements buffer

- ₹10 → Running cost: team + tools + compliance basics

- ₹15 → Contribution left (this is what funds growth buffer, experiments, and eventually profit)

Now convert that into the thing founders actually feel: cash timing.

A typical “cash pain” sequence looks like this (illustrative):

- You pay packaging + raw material before the unit sells (cash out first).

- You pay manufacturing/packing around production (cash out again).

- You pay marketing weekly/daily (cash out constantly).

- You sell the unit… and if you sold through offline or marketplaces, you get paid later (cash comes back last).

So even if the unit economics are fine on paper, the bank balance can stay tight because the cash cycle is longer than the growth cycle.

That is the real takeaway: in a young BPC brand, money doesn’t only “go” into COGS. It goes into shelves, trust, movement, and then it gets trapped in time.