In the early 2000s, an entrepreneur in Palo Alto could raise a million dollars based on a whiteboard sketch, a Stanford degree, and a compelling vision of scale. Around the same time, in a crowded Bengaluru workspace, a founder was more likely to be asked for a three-year EBITDA projection before their first pilot was complete. These two scenes capture the historical essence of Silicon Valley and India’s startup ecosystem.

While Silicon Valley has long been the North Star of global innovation, India’s startup ecosystem has ceased to be merely a reflection of the West. By 2026, the gap between the two is no longer about who is ahead, but about how differently they create value. Silicon Valley builds for the next frontier of technological possibility. India builds for the next billion people entering the formal economy. Both ecosystems solve hard problems, but under very different constraints, incentives, and timelines.

Different Starting Lines

When Silicon Valley took its first entrepreneurial steps in the 1960s and 1970s, India remained a largely closed economy. Stanford University was already spinning out semiconductor companies like Hewlett-Packard and Intel, supported by US defence research funding, public R&D grants, and a growing venture capital industry designed for long-horizon risk-taking. By the time Apple was founded in 1976, Silicon Valley had universities, capital pools, research labs, and early public-market pathways working in tandem.

India’s startup story began much later and under very different conditions. Until the early 2010s, entrepreneurship was fragmented and often necessity-driven. Capital was scarce, failure was stigmatised, exits were rare, and regulatory friction slowed and complicated the formation of companies. Much of India’s best technology talent either joined large IT services firms or migrated abroad, particularly to the US.

This imbalance began to change meaningfully in the last decade.

In 2016, the Government of India launched the Startup India initiative to formalise entrepreneurship, reduce friction, and position startups as engines of employment and economic growth. The programme focused on easier incorporation, tax exemptions, faster IP processing, access to seed funding, and state-level startup policies, without attempting to replicate Silicon Valley’s research-heavy model.

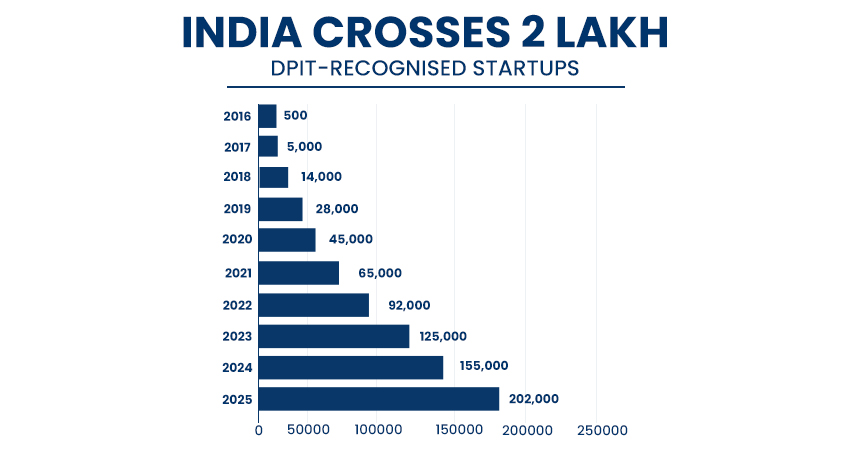

The impact was significant. India went from a few hundred recognised startups in 2016 to over 200,000 DPIIT-recognised startups by 2025, making it one of the world’s largest startup ecosystems by count. Startup formation spread beyond metros into Tier II and Tier III cities, increasing geographic participation, even though quality and depth remained uneven.

Unlike Silicon Valley, which evolved over five decades, India compressed the growth of its ecosystem into less than 10 years. Speed replaced depth. Scale arrived before maturity. Policy and digital infrastructure played a disproportionately large role in shaping outcomes.

This compression produced a fundamentally different entrepreneurial DNA, one shaped less by abundance and more by constraint.

Cultural DNA: Optimism Versus Resilience

Silicon Valley’s culture is rooted in optimism and risk tolerance. Failure is treated as learning, and capital markets reward bold vision. In 2025, the United States remained the world’s largest startup ecosystem, hosting 96,000+ startups and 630+ unicorns, with an ecosystem growth rate of 18.2%. This density of capital and exits reinforces the belief that speed, category leadership, and scale matter more than early profitability.

This mindset is visible in how US startups scale. Companies like Instagram and WhatsApp achieved massive user adoption with minimal revenue pressure before billion-dollar acquisitions. Even today, frontier GenAI startups raise capital primarily on vision, talent density, and technical ambition. Multi-billion-dollar funding rounds for companies such as OpenAI and Anthropic highlight how capital-intensive Silicon Valley’s frontier bets have become. Crunchbase

India, by contrast, evolved under capital scarcity. Founders operate in markets defined by price-sensitive consumers, fragmented distribution, and limited access to late-stage capital. As a result, the ecosystem prioritises lean execution and early validation. By 2025, more than 11,000 Indian startups had shut down, reflecting a broader shift away from “growth at all costs” toward sustainable business models. This shift is reinforced by corrected Tracxn data, which shows that 724 startups shut down in 2025 (till October), a sharp decline from 3,903 closures in 2024.

This pressure produced a different founder archetype. Companies such as Zoho and Freshworks prioritised profitability early, often bootstrapping for years while building globally competitive SaaS products. Capital discipline, resilience, and operational clarity became India’s competitive edge.

Government Policy: Research Backbone Versus Ecosystem Builder

Government policy is one of the most misunderstood differences between the two ecosystems.

In the United States, there is no single flagship programme equivalent to Startup India. Instead, the government plays a quieter but structurally powerful role. Federal R&D funding through programmes such as SBIR and STTR provides non-dilutive capital to early-stage startups in deep tech, healthcare, and defence-linked innovation. Many leading US technology companies trace their origins to publicly funded research.

R&D tax credits further reduce the cost of innovation, while legislation such as the CHIPS and Science Act and the US Innovation and Competition Act commits tens of billions of dollars toward semiconductors, AI, and advanced manufacturing. The state acts as a long-term risk absorber rather than an ecosystem operator.

India’s approach has been more direct and infrastructure-led. Startup India focused on lowering entry barriers rather than funding frontier research at scale. In parallel, India invested heavily in Digital Public Infrastructure. Platforms such as Aadhaar, UPI, DigiLocker, and ONDC transformed essential digital rails into public goods. By the end of 2025, UPI was processing over 21.6 billion transactions per month, making India the world’s largest real-time payments ecosystem.

This fundamentally altered startup economics. Fintech companies no longer need to build payment infrastructure. They competed instead on trust, user experience, and value-added services. For consumer startups, this meant lower transaction costs, faster onboarding, and national reach without owning infrastructure.

However, limitations persist. Grant access remains bureaucratic, compliance burdens continue, and funding for deep research remains modest compared to the US.

Investment Philosophies: Risk Depth Versus Capital Efficiency

Silicon Valley’s defining advantage remains the depth and patience of risk capital. Over 60% of global venture capital dry powder is concentrated in North America, enabling funds to underwrite risk for a decade or more. This structure supports pre-revenue, research-heavy innovation in areas such as foundational AI, biotech, semiconductors, and advanced materials.

Companies like SpaceX, Moderna, and OpenAI benefited from multiple funding cycles before reaching meaningful revenue or market validation, an approach that is structurally difficult in most other ecosystems.

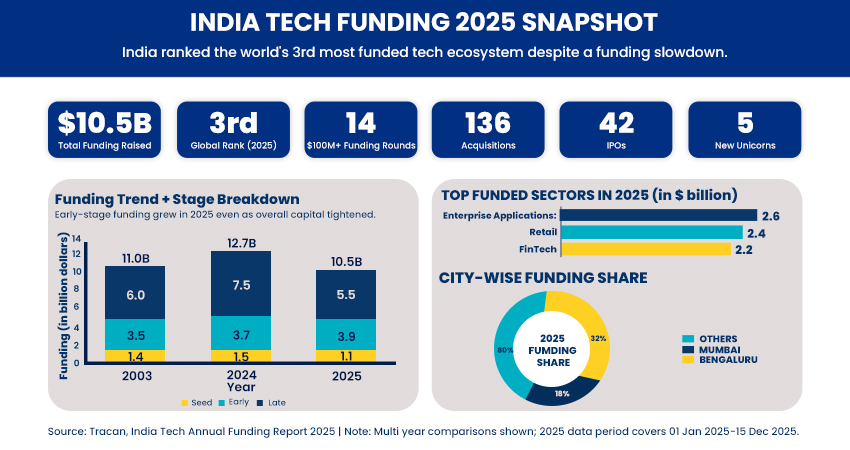

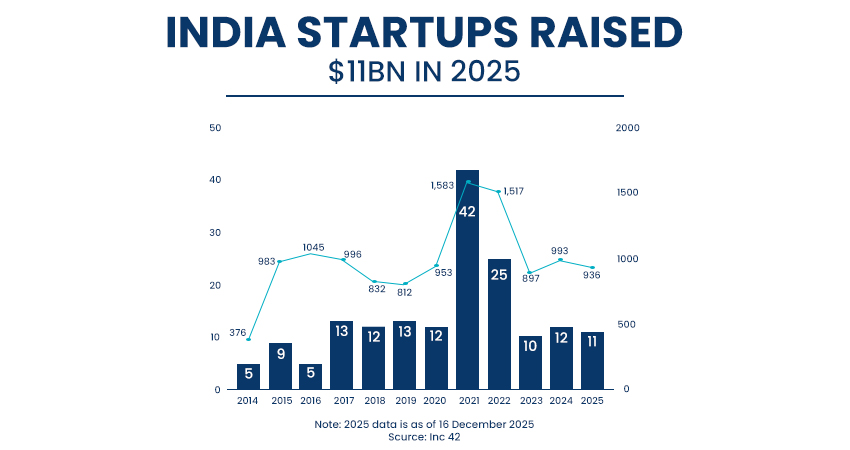

India’s venture ecosystem remains more constrained in both depth and time horizon. Startup funding declined from $12.7 billion in 2024 to approximately $11 billion in 2025, with the sharpest impact at the Seed and Series A stages, particularly in consumer and D2C categories. Smaller fund sizes and earlier exit pressure naturally push investors toward faster monetisation and clearer paths to profitability.

The upside of this constraint has been higher capital efficiency and stronger unit economics. The downside is slower progress in frontier technologies that demand patient capital and long development cycles, such as semiconductor design, deep biotech, or foundational AI research.

Founder Mindset: Vision-Led Versus Constraint-Bred

Founder behaviour in Silicon Valley and India is shaped less by personality and more by ecosystem design.

Silicon Valley founders are encouraged to think in terms of category creation and global scale from day one. Narrative strength, technical pedigree, and conviction often outweigh immediate traction. Companies like Airbnb and Stripe scaled for years before optimising for profitability.

Indian founders are shaped by constraint. Limited capital, price-sensitive consumers, and operational complexity push founders toward early validation and execution discipline. Vision alone rarely secures funding. Companies like Razorpay, Delhivery, and Lenskart scaled by mastering operations, distribution, and cash-flow visibility.

Indian founders tend to build resilient, operationally sound businesses, while Silicon Valley produces audacious bets with higher failure rates. The next phase of India’s ecosystem may depend on founders who can blend ambition with execution.

Consumer Behaviour: Convenience Versus Necessity

Consumer behaviour further shapes outcomes.

Silicon Valley products optimise for incremental convenience in already mature digital markets. India’s market is fundamentally different. With nearly 950 million internet users, many of whom are entering the digital economy for the first time, adoption is driven by necessity rather than novelty. Business Standard

This is why Indian consumer brands scale differently. Companies such as Mamaearth and mCaffeine grew by solving climate-specific and locally relevant problems. India’s D2C market was valued at $87.5 billion in 2025 and is projected to reach $322 billion by 2031, growing at a CAGR of over 24%.

Indian brands are also phygital by default. Companies like Lenskart and boAt invested early in offline retail, recognising that trust in India is still built physically, not purely digitally.

Talent and the Reverse Brain Drain

For decades, Silicon Valley was the primary magnet for Indian engineering talent. It continues to lead in foundational AI, semiconductors, and advanced research, thanks to a dense network of universities, labs, and capital.

However, this flow is now rebalancing. Companies like Postman, Freshworks, and Chargebee have demonstrated that global SaaS businesses can be built from India. By mid-2025, a 3.7× surge in startups positioned India as the world’s second-largest Generative AI startup hub, with the ecosystem growing to over 890 GenAI startups. This marks a clear shift from execution-led roles toward innovation-driven ambition.

Startups such as Sarvam AI and Krutrim are now building India-first foundational models rooted in the local context while aiming for global relevance.

Where India Still Lags and Why Silicon Valley Continues to Lead

Despite rapid scale and recent policy shifts, structural gaps persist that keep Silicon Valley at the forefront of frontier innovation.

- Shortage of Patient Risk Capital: Silicon Valley benefits from massive, long-duration “dry powder” that absorbs high failure rates. In contrast, Indian investors often seek immediate revenue and domestic market fit, creating a “valley of death” for deep tech startups that require three to five years of R&D before a single successful pilot.

- Infrastructure and Compute Gap: While India has launched the Semiconductor Mission 2.0, it still lacks the decades of accumulated hardware infrastructure and hyperscale compute clusters found in the US. This forces Indian deep tech firms to rely on foreign fabs and overseas cloud credits, increasing operational costs and slowing iteration.

- Weak Institutional Commercialisation: US universities like Stanford and MIT have robust pipelines for spinning off research into startups with clean IP ownership. In India, academia-industry collaboration remains fragmented, with many promising innovations getting stuck in labs due to bureaucratic IP deadlocks and a lack of institutional licensing bridges.

Absence of “Deep Pockets” for Moonshots: Silicon Valley leads in capital-intensive bets like foundational AI and orbital robotics because it has private funds willing to invest billions into pre-revenue ventures. Indian funding remains largely concentrated in the application layer and quick-commerce, making it difficult to fund indigenous, multi-year technological breakthroughs.

A Multi-Polar Startup Future

The comparison between Silicon Valley and India is often framed as a race. In reality, it is a story of divergence.

Silicon Valley remains the world’s laboratory for frontier innovation, answering the question of what is technologically possible next. India has become one of the strongest engines for making innovation economically viable at scale, answering the questions of what is workable, affordable, and scalable.

A single geography will not dominate the global startup economy. It will be multi-polar. The winners will be those who can deploy technology profitably, inclusively, and at cultural scale.

In that future, Silicon Valley and India are not competitors. They are complementary forces shaping different chapters of the same global innovation story.